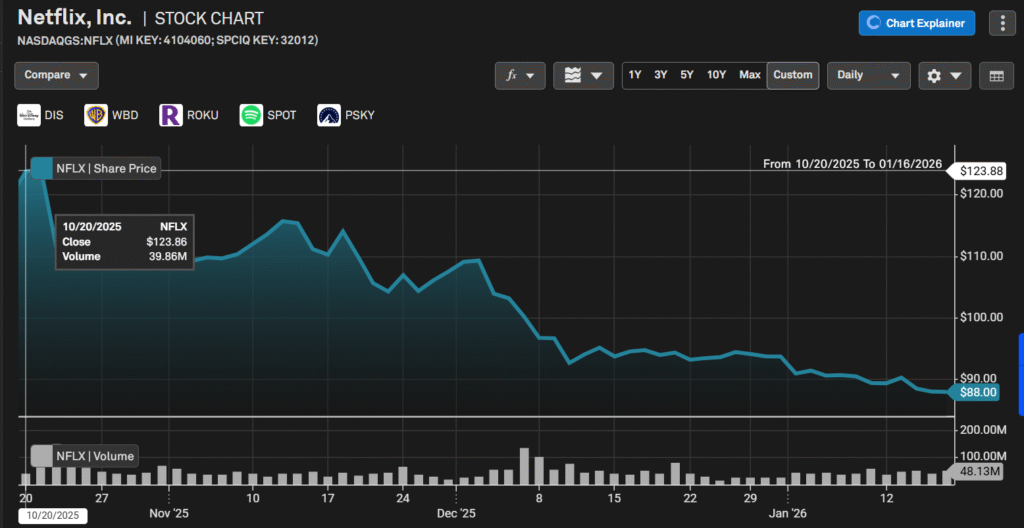

Netflix (NFLX) has declined ~29% over the past three months, driven largely by market concerns surrounding its proposed acquisition of Warner Bros. Discovery (WBD). This is widely viewed as a bold attempt to accelerate consolidation within the global streaming industry, but it has been met with investor skepticism, with many viewing the premium bid as a significant overpay.

Source: Capital IQ Pro, Netflix stock data

This has led to uncertainty around capital allocation, and regulatory scrutiny weighed on the stock. According to the Financial Times, Netflix has tabled an all-cash offer of approximately US$82.7bn, intensifying concerns over balance-sheet strain.

As a result, NFLX has meaningfully underperformed. But here’s why we are taking the contrarian stance, buying amidst everything.

Equity is King

The decision from upper management switching to an all-cash bid subtly indicates that they view the current market valuation of their stock does not fully reflect its intrinsic value, being undervalued. More notably, the senior-management’s compensation is largely equity-linked. Their net worth and wealth is virtually tied directly to stock price.

If management viewed the stock as fairly valued or overvalued, they would willingly dilute shareholders by issuing equity, as equity would be a comparatively cheaper form of consideration than cash. Equity compensation is tied to the stock price. Any subsequent decline in the share price would reduce the economic cost of the deal.

Vice Versa, management’s decision to proceed with an all-cash bid signals clear reluctance to part with equity at current price levels. We see this as management viewing the company’s shares as undervalued relative to intrinsic value, making equity a more costly form of consideration than cash. In summary, management rather uses pure cash than part with equity they view as undervalued.

Cash is the Signal

With earnings around the corner, management would have had a clear view into the company’s near-term financial performance and balance-sheet position. Their willingness to commit to an all-cash offer of such a magnitude suggests that the decision was made with a high degree of financial consideration, reflecting confidence in their underlying financials.

This is supported by Netflix’s trend of strong free cash flow generation in the prior year, which demonstrates the company’s ability to fund strategic initiatives without placing excess strain on its balance sheet.

More importantly, offering such a sum implies that management expects the transaction to be serviceable through future operating cash flows, rather than placing undue strain on the company’s financial position.

Concise Summary & Base Case

In summary, we expect Netflix’s share price to react positively post-earnings. This is supported by solid operating performance and continued confidence in underlying fundamentals from management’s actions during this bidding war.

With regards to the bidding war, we do not foresee Netflix to significantly outbid Paramount Global. Instead of prolonging the aggressive bidding war, Netflix is likely to rely on its strong balance sheet and financial credibility, keeping the bidding relatively controlled. If Netflix wins the asset, it will likely do so a disciplined premium. If the price rises beyond what makes financial sense, we think Netflix would walk away, allowing competitors to potentially overextend themselves. This strategy maintains capital discipline while preserving upside potential.